As the disclosure of the 2022 midterm report of listed companies is nearing the end, more photovoltaic enterprises have disclosed their performance in the first half of the year, and the performance has almost increased.

Red Star Capital Bureau found that some photovoltaic enterprises located in the upper and middle reaches no longer follow the "specialization" development path, but instead extend the industrial chain upstream and downstream, and take the "vertical integration" development path.

↑ Photovoltaic Industry Map IC Photo

"Vertical integration development" becomes a trend

The upstream winner takes all, and the downstream may become a substitute factory

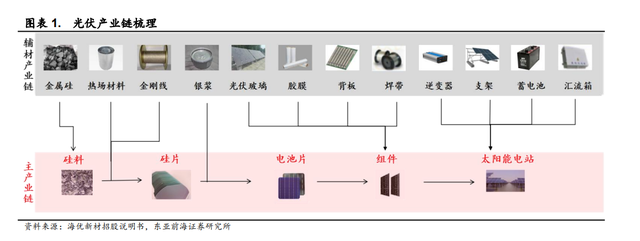

From the perspective of connecting the entire photovoltaic industry chain, there are five main links from the upstream to the downstream, namely: silicon material - silicon chip - battery chip - module - solar power station.

↑ Screenshot from the research report of East Asia Qianhai Securities

In the past, there have been disputes on the development path of photovoltaic enterprises in the industry:

Some people think that photovoltaic enterprises should follow the "professional" development path, focusing only on one of the links; However, some people believe that the development path of "vertical integration" should be followed, and the production line of the enterprise itself covers the entire photovoltaic industry chain.

However, Red Star Capital Bureau noted that this dispute seems to have an answer this year.

With the price of silicon material rising to more than 300000 yuan/ton, there is a view in the industry that silicon material has squeezed the profit space of the downstream of the industrial chain, and even upstream enterprises have made strong inroads into the downstream component links.

Take Tongwei (600438. SH) as an example. As one of the "silicon faucets", it also has a layout in the fields of battery chips, components, etc. Especially in the middle of August, its subsidiary became the first candidate to win the bid for a large component order of a central enterprise, which was also seen as a signal of its strong entry into the component sector. (For details, see the previous report "Tongwei Shares enter the component link, or will monopolize the centralized purchase orders of central enterprises at a low price, and the component shares will plummet collectively")

At present, Tongwei has an annual production capacity of 230000 tons of high-purity crystalline silicon and 54GW of solar cells. In the first half of this year, Tongwei's net profit attributable to the parent company was about 12.224 billion yuan, a year-on-year increase of about three times.

In contrast, Daquan Energy (688303. SH), which is also a "silicon leader", has slightly less profit attributable to the parent company. According to the announcement, Daquan Energy's production capacity of high-purity polysilicon is 105000 tons/year, and its output in the first half of this year is 66700 tons. Its net profit attributable to the parent company is about 9.525 billion yuan, an increase of about 3.4 times year-on-year.

Midstream enterprises extend the industrial chain

The "Four Diamond" module was launched, and Jinko won the championship

Not only is it the upstream "silicon leader", Red Star Capital Bureau noted that photovoltaic enterprises in the middle reaches are also continuing to extend the industrial chain downward, such as TCL Central (002129. SZ), one of the "duopoly" in the silicon chip sector.

Red Star Capital Bureau found that in 2021, photovoltaic silicon chip products contributed 77.35% of TCL Central's revenue, while photovoltaic module products only contributed 14.89%.

On June 29, TCL Zhonghuanfa announced that its holding subsidiary, Huansheng New Energy (Jiangsu) Co., Ltd., would be invested by 1 billion yuan as the main body of the project to invest in the construction of the annual production of 3GW efficient laminated solar cell module project and the construction of G12 efficient laminated production line and supporting facilities.

Like Tongwei, TCL Central's move is also interpreted by the outside world as "extending the industrial chain".

According to the financial report disclosed recently, TCL Central's revenue in the first half of the year was 31.698 billion yuan, up 79.65% year on year; The net profit attributable to the parent company was 2.901 billion yuan, with a year-on-year growth of about 92.10%.

Another "oligarch" in the silicon chip sector is Longji Green Energy (601012. SH). It should be noted that Longji Green Energy produces both silicon chips and components.

↑ Component products of Longji Green Energy, screenshot from its official website

According to incomplete statistics of Red Star Capital Bureau, the top four listed companies are ranked according to the shipment volume of components, as follows:

Jinko Energy (688223. SH) sells about 18.21GW of components worldwide. The revenue in the first half of the year was about 33.407 billion yuan, with a year-on-year growth of 112.44%; The net profit attributable to the parent company was about 905 million yuan, up 60.14% year on year.

The photovoltaic products of Trina Solar (688599. SH) are photovoltaic modules, with 18.05GW shipped in the first half of the year. The revenue in the first half of the year was about 35.731 billion yuan, up 76.99% year on year; The net profit attributable to the parent company was about 1.269 billion yuan, up 79.85% year on year.

Longji Lvneng achieved 18.02GW of component shipments. The revenue in the first half of the year was about 50.417 billion yuan, up 43.64% year on year; Net profit attributable to the parent company was about 6.481 billion yuan, with a year-on-year growth of 29.79%

The component shipment of JA Technology (002459. SZ) is 15.67GW. The revenue in the first half of the year was about 28.469 billion yuan, up 75.81% year on year; The net profit attributable to the parent company was about 1.702 billion yuan, with a year-on-year growth of 138.64%.

It is worth mentioning that enterprises such as Jingao Technology also have the production capacity of the whole photovoltaic industry chain from crystal pulling to silicon wafer to battery module.

Few downstream enterprises extend the industrial chain

Brokers: All midstream manufacturers adopt vertical integration

The downstream of photovoltaic industry is solar power station. Among them, the inverter is the key equipment in the power generation system, which can convert the variable DC output to AC, and can directly affect the power generation efficiency.

In this link, the listed companies involved mainly include Sungrow Power (300274. SZ) and TBEA (600089. SH).

Among them, the revenue of Sungrow Power in the first half of this year was about 12.281 billion yuan, with a year-on-year growth of 49.58%; The net profit attributable to the parent company was about 900 million yuan, with a year-on-year growth of about 18.95%. Sungrow Power attributed the growth of revenue to the growth of inverter and energy storage business.

The revenue of TBEA in the first half of the year was about 3.872 billion yuan, with a year-on-year growth of about 72.15%; The net profit attributable to the parent company was about 6.905 billion yuan, with a year-on-year growth of about 122.29%.

After sorting out, Red Star Capital Bureau found that photovoltaic enterprises located in the downstream rarely extended the industrial chain, and their revenue and net profit attributable to the parent company did not grow as fast as upstream and midstream enterprises.

Zhongyuan Securities also said in the recently released comment report on the photovoltaic industry that, in order to ensure the stability of the supply chain and achieve the maximum profit interception of the industrial chain, the main photovoltaic midstream manufacturers all adopt the vertical integration mode to achieve the extension to the upstream or downstream.

Red Star Journalist Yang Peiwen

Edited by Yu Dongmei and Yang Cheng